Most cash advance apps are designed to give you quick access to money before payday, and some offer separate products that actually help you build credit. If your goal is more than just covering a short-term expense, it’s important to choose an app that also offers a product that reports repayment activity to the major credit bureaus. That way, you’re not just borrowing, you’re creating a track record that could improve your financial future.

We’ll cover the best cash advance apps that can also help you build credit. You’ll also learn how they work, what to look for and how to decide if they’re right for you.

Do cash advances actually report your cash advance repayment activity?

No, a cash advance by itself does not affect your credit history. We couldn’t find any apps that report on-time cash advance repayments to the credit bureaus.

However, some cash advance apps also offer credit-building loans or lines of credit tied to your account, which can help you build credit.

Hot tip: Look for apps that report to all three major credit bureaus (Experian, Equifax, TransUnion), which gives you the broadest impact.

Best cash advance apps offering credit-building products

Here’s a quick comparison to help you see which apps offer products that actually report and what makes them different.

| Current | Secured credit card (“Build Card”) | All 3 bureaus | Rewards points + round-up savings |

|

| Brigit | Credit-builder loan | All 3 bureaus | Includes smart budgeting tools |

|

| Cleo | Credit-builder card | All 3 bureaus | AI chatbot for budgeting + advances |

|

| EarnIn | Secured credit card | All 3 bureaus | Balance Shield overdraft alerts |

|

| MoneyLion | Credit-builder loan and credit builder plus | All 3 bureaus | Bundled with RoarMoney account |

|

| Possible Finance | Installment loan + credit card | TransUnion and Experian | Flexible installment repayment |

|

| Varo | Secured credit card and line of credit | All 3 bureaus | No interest, no annual fee |

|

| Albert | Credit-building loan (“Albert Instant”) | All 3 bureaus | Paired with “Albert Genius” financial guidance |

|

| Dave | Credit-building loan (“LevelCredit”) | All 3 bureaus | Combines ExtraCash advance + Side Hustle job matching |

|

| Tilt | Credit line | All 3 bureaus | Larger advance limits than most apps |

|

| Kikoff | Credit account + secured card | All 3 bureaus | Low fixed monthly plan |

How to choose the right app

Not every credit-reporting cash advance app works the same way. Before signing up, think about how the product fits your lifestyle and goals:

- Type of credit-building product. Some apps, like Varo or Current, offer secured credit cards that report your regular purchases. Others, like MoneyLion or Brigit, use credit-builder loans where you make monthly payments toward savings. Choose the format that feels easiest to stick with.

- Repayment style. A credit-builder loan usually has fixed payments, which can be helpful if you like predictability. Secured cards and lines of credit are more flexible, but that flexibility can tempt overspending if you’re not careful.

- Credit bureau coverage. Some apps only report to one or two bureaus, which limits your impact. Look for products that report to all three (Experian, Equifax, TransUnion) so you get the broadest credit lift.

- Account or subscription requirements. Certain credit-building tools are only available if you pay for a premium membership or open a linked checking account. Factor in whether the extra cost is worth the potential credit benefits.

- Advance vs. credit building. Remember that the advance feature and the credit-building feature are separate. An app that’s great at delivering fast cash may not be the strongest option for building long-term credit.

Hot tip: If your main goal is credit improvement, make sure you’re not paying more in fees than the credit-building is worth.

Typical eligibility requirements for credit-building products in cash advance apps

These requirements are not necessarily required to access the app or cash advance alone, but to qualify for the credit-reporting products:

- Checking account requirements. Most apps require you to link a bank account where payments can be auto-drafted.

- Direct deposit or income minimum. Some apps set a minimum to prove repayment ability.

- Credit score. Most don’t require good credit since they are designed for people rebuilding, but they may still do a soft credit check.

- Residency & ID verification. You need to be a US resident with a valid ID and Social Security number.

- Subscription or account upgrade. Some apps, like Brigit or MoneyLion, only unlock credit builder loans if you pay for a subscription or open a linked account.

Hot tip: Even if apps don’t require a strong credit score, they still need proof of steady cash flow. If your income is inconsistent, you may have trouble qualifying for any credit-building features.

How much do reported on-time payments raise my credit score?

While there’s no fixed formula for how much your credit score will rise, consistently reported on-time payments can significantly improve it over time. Payment history accounts for about 35% of your FICO score.

When payments are treated like installment loans and reported on time, they strengthen your payment history and are often the biggest factor in improving your score. Exact point increases vary by credit profile, but positive installment repayments reported consistently can gradually help lift your score over several months.

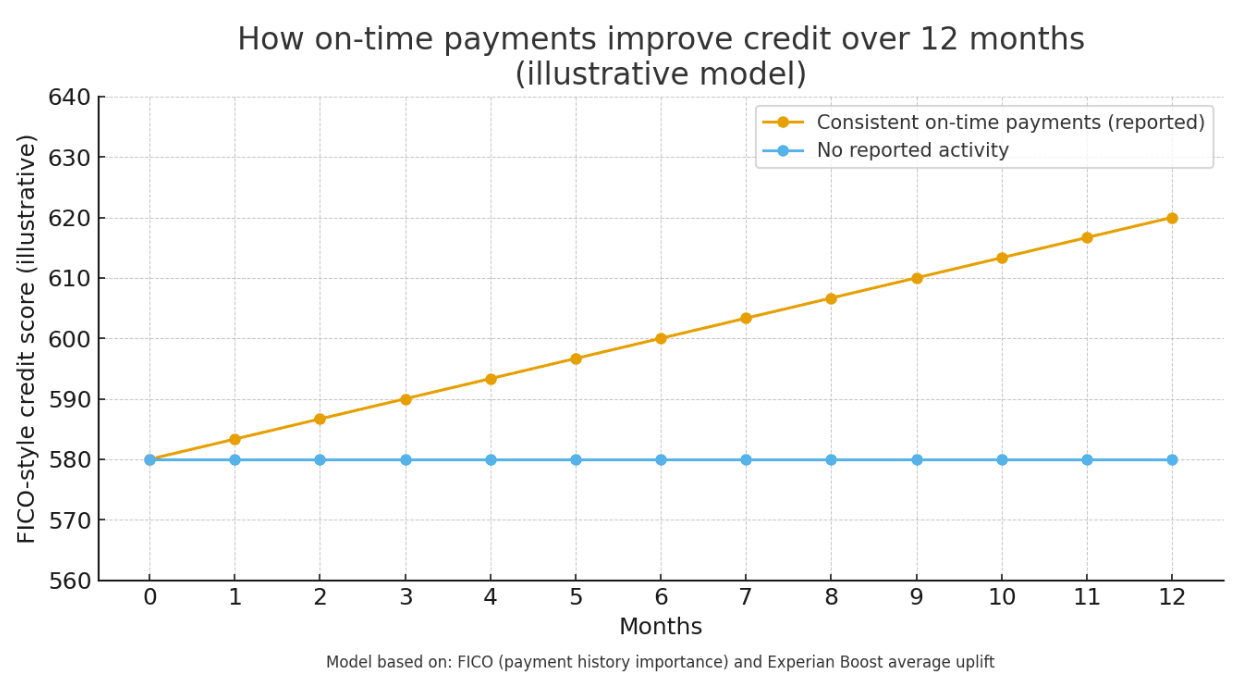

How on-time payments improve credit over time

This chart shows an illustrative example of how a credit score could rise over 12 months with reported on-time payments compared to no reported activity, using insights from FICO and Experian Boost data.

While exact results vary by person, the takeaway is clear: If the lender reports your payments, your score can move upward over time.

Things to watch out for

While credit-reporting apps can help, there are trade-offs to be aware of.

- Some require monthly subscription fees, though some apps are mostly free.

- Advance amounts and loans are usually small.

- Missed or late payments can hurt your credit instead of helping it.

- Not all apps have products that report to all three credit bureaus.

Alternatives to cash advance apps for building credit

Cash advance apps aren’t your only option. Other tools may offer lower costs or broader benefits:

- Secured credit cards. You put down a deposit, and your on-time payments are reported like a regular credit card.

- Credit-builder loans. Many community banks and credit unions offer these small loans, which build credit while you save.

- Rent and utility reporting services. Adding rent or utility payments to your credit report can help you build history without taking on new debt.

- Personal loans (if you qualify). Traditional personal loans from banks, credit unions or online lenders often report to all three credit bureaus. On-time payments can boost your score, but approval usually requires stronger credit or income.

Bottom line

If you’re only looking for fast cash, almost any cash advance app can help. But if you want to build credit at the same time, your options are more limited. Be sure to compare the actual credit-building product it offers.

Before choosing, think about whether you want simple early wage access or a structured path to improve your credit history. The right choice can give you relief today and set you up for stronger financial opportunities tomorrow.

Frequently asked questions

")